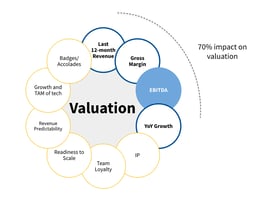

After the top four value drivers (Growth rate, Revenue, Gross Margin, and EBITDA), we want to...

We have talked about the two most important attributes that drive ETS valuations: Growth rate and Revenue. The next metric is extremely timely to talk about with the current economic headwinds because it is the key indicator to the value of the offerings to the customer: gross margin. The gross margins are the one feature that differentiate ETS from any other services companies. They are the key indicator that your service is in fact a differentiated offering. In strict financial terms,

Gross Margin (%) = (Revenue - Cost of Goods Sold (COGS)) / Revenue

That is, it is the percentage or revenue left after paying off all costs related to delivery of the said revenue. In the case of ETS startups, COGS is the cost of any talent and any tools deployed to deliver a service to a customer. Gross Margin (GM) can be measured across time and across scopes, e.g., it can be measured for a given time period, or measured on a per-customer, per-project, or per-service.

As we said in our blog post on Demystifying ETS Valuations: Growth, growth is a critical component of success in ETS business. Gross margins are the counter-measure to ensure the business doesn’t grow into a place where, as the joke goes, they are “selling at a loss but will make it up on volume”. Checking the gross margins ensures the revenue is not artificially inflated by making bad deals. Growth and gross margin, while not at odds, can be seen as a trade off. For example, pricing can be lowered to win a deal but it is important to ensure that such a discount does not drive gross margin so low that the revenue increase is no longer worth it for the business. Balancing growth with gross margin is what signals a truly strong ETS business.

Side note on how to measure GM: When you’re growing you’ll have to pay for growth by hiring ahead – because having people available to close a deal is more important than conserving cash. This bench cost should not be included in the COGS as it is a cost of growth. Thus, the best way to measure and report GM is on a per-project basis where both revenue and costs are computed for a given project.

Commoditized businesses often have very low gross margins. When many vendors offer the same or similar services, customers have more power to negotiate and this allows them to drive down the price, which shrinks gross margin. A high GM generally indicates that the company has a unique value proposition, quality talent and a smooth customer experience, which is what allows them to charge high gross margins. Gross margins are the best indicator of a business’ profile/intent. Founders who are thinking of building a commodity business for cash will often charge the minimum possible gross margins to sustain. Consequently, they get categorized as a commodity which allows customers to further drive their margins lower. This generally leaves no “spare” money on the table to invest in strategic initiatives like developing technical or marketing IP, sharpening value propositions, or improving delivery processes. Consequently, the business keeps getting marginalized.

Low Gross Margin Loop

Low Gross Margin LoopA true ETS startup should have a unique value proposition and build a strong customer reputation, that allows them to charge premium pricing – leading to a high GM. Higher GM creates a nice positive cycle for ETS startups – high GM means they have more dollars they can invest in their processes, IP, and hiring and training employees ahead. As a result, they are able to further improve their value proposition and customer experience, which then allows them to charge even higher gross margins, and so on and so forth. Such businesses continue to command premium pricing and keep going higher and higher in their value propositions.

High Gross Margin Loop

High Gross Margin LoopWhen it comes to valuation, higher GM is rewarded for three reasons. First, it indicates financial opportunity. A very popular investment thesis is to buy a services business and reduce its SG&A costs and invest in increasing revenue to make the business more profitable. Second, it indicates the quality of talent. A common reason ETS companies are acquired is for its talent and a strong GM indicates a strong team that people are willing to pay for. Third, it indicates a strong competitive position in the market which implies lower risk of future revenue.

A lower GM is often not just penalized in valuation, but can turn off many potential investors/buyers because it indicates a business with commoditized branding. Such businesses are acquired for different reasons like expanding footprint and valued as a commodity at 0.5-1x revenue.

Increasing gross margins requires the founders of the startup to adopt the mindset of a truly differentiated business. You have to sharpen the vision and get out of the revenue grind of just getting the next dollar of revenue. A good strategy is to attach to an ecosystem where growth is high and the supply to talent is shorter than the demand. Next, create a clear view of your ideal customer profile, your services, and then stop deviating from it when looking for customers. Say no when a customer is not matching your requirements. With a clear services portfolio, target your ideal customers and price yourself right, without fear. You will hear more frowns than you may like but hold your ground, and work with the few customers that understand your value proposition and are willing to pay a good price. These customers will help you shape your offerings and enable you to build few high-quality services that you can then turn around and charge more for down the road. As you earn the gross margin, focus on reinvesting it in the business to further differentiate yourself with better talent, technical IP, services, and/or credentials. This allows you to kickstart the high gross margin cycle.

At Vixul, this is one of our hypotheses that Emerging Technology Services businesses can be built better with a differentiated, value-focused mindset. Thus, one of the things we help founders with is creating more differentiated offers so that they can commend higher gross margins. Learn more about Vixul on vixul.com or contact us to have a discussion on how we can help.

The other articles in our "Demystifying ETS Valuations" series are:

-

Demystifying ETS Valuations Part 4: EBITDA and the rule of 40

-

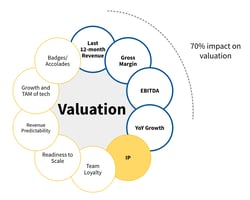

Demystifying ETS Valuations Part 5: Intelectual Property

-

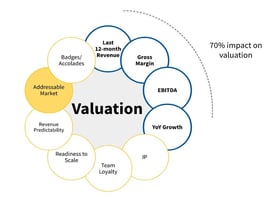

Demystifying ETS Valuations Part 6: Addressable Market

-

Demystifying ETS Valuations Part 7: Revenue Predictability

-

Demystifying ETS Valuations Part 8: Team Loyalty

-

Demystifying ETS Valuations Part 9: Badges And Accolades

-

Demystifying ETS Valuations Part 10a: Readiness To Scale

-

Demystifying ETS Valuations Part 10a: Readiness To Scale